What Foreign-Owned U.S. Corporations Must Know

$25,000.

That is the starting penalty for failing to properly file Form 5472.

For foreign-owned U.S. corporations and foreign-owned disregarded entities, this is not a theoretical risk. It is a statutory enforcement mechanism under Internal Revenue Code Section 6038A and 6038C.

Most taxpayers do not fall into this trap because they are hiding income.

They fall into it because they misunderstand structure.

Who Must File Form 5472

Form 5472 applies to:

- U.S. corporations that are at least 25% foreign-owned

- Foreign corporations engaged in a U.S. trade or business

- Foreign-owned U.S. disregarded entities, including single-member LLCs

Many foreign entrepreneurs set up U.S. LLCs believing they have no filing obligation if there is no taxable income. This misunderstanding frequently overlaps with broader international reporting issues such as those explained in FinCEN Form 114 vs Form 8938.

Ownership structure matters more than profit.

The Pro Forma Form 1120 Requirement

Foreign-owned U.S. disregarded entities must:

- File a pro forma Form 1120

- Attach Form 5472

- Submit by the applicable due date, including extensions

They cannot e-file Form 5472.

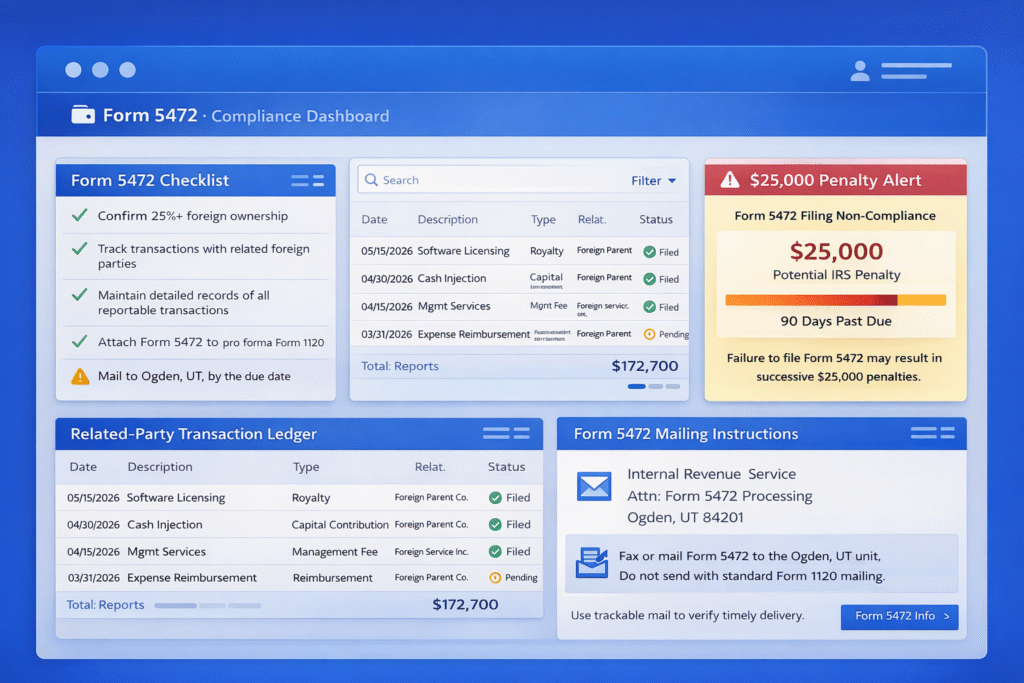

The filing must be mailed or faxed to the designated IRS unit in Ogden, Utah. Sending it to a standard Form 1120 processing address is a common mistake that results in “missing” filings and subsequent penalty notices.

Procedural mistakes are one of the biggest triggers of penalties.

For a deeper breakdown of entity-level exposure, see our article on Form 5472 Filing Requirements for Foreign-Owned U.S. Entities.

What Counts as a Reportable Transaction

There is no meaningful minimum threshold.

Common reportable transactions include:

- Capital contributions

- Loans between entity and foreign owner

- Expense reimbursements

- Management or service fees

- Intercompany purchases

- Informal transfers between accounts

Even routine funding transfers can trigger reporting.

This becomes especially relevant in multi-entity environments, where related-party structuring overlaps with areas such as those discussed in our guide to CPA Guide to M-1 Adjustment Journal Entries.

The absence of taxable income does not remove reporting obligations.

The $25,000 Penalty Structure

The penalty is automatic.

Base Penalty

Failure to properly file Form 5472 results in:

- $25,000 per required form

This applies to:

- Late filings

- Substantially incomplete filings

- Failure to maintain required records

Escalation After IRS Notice

If the failure continues more than 90 days after IRS notice:

- An additional $25,000 penalty applies

- For each 30-day period or part thereof

- Potentially per related party

Total Potential Exposure

Scenario | Penalty Exposure |

1 year missed filing | $25,000 |

2 consecutive years missed | $50,000 |

3 consecutive years missed | $75,000+ |

Failure continues after IRS notice | Additional $25,000 per 30 days |

Multiple related parties involved | Separate penalties possible |

The exposure compounds quickly.

If your clients also face overlapping reporting requirements, exposure may connect to areas such as Form 1099 Filing and Reporting Guide.

The Farhy Decision and IRS Authority

There was temporary uncertainty when the Tax Court in Farhy questioned whether the IRS had authority to summarily assess certain international penalties.

However, the D.C. Circuit Court reversed that decision, reaffirming the IRS’s power to automatically assess Section 6038A penalties.

For 2026, there is no ambiguity.

The IRS can assess these penalties directly.

Procedural arguments do not eliminate liability.

The Transparency Gap After CTA Changes

In March 2025, the Corporate Transparency Act enforcement posture shifted for certain domestic entities.

While CTA penalties were structured at $500 per day, enforcement priorities evolved for U.S. persons.

Form 5472 did not change.

This creates a transparency gap.

Ownership reporting may have shifted under Treasury policy, but related-party transaction reporting under Section 6038A remains fully active.

For foreign-owned U.S. businesses, Form 5472 is now the primary federal transparency instrument.

The Real Trap Is Technical

Most failures occur due to three misunderstandings:

- The 10% attribution ownership rules

- The absence of a de minimis transaction threshold

- The inclusion of foreign-owned disregarded entities since 2017

Additionally, penalties may be imposed for failing to maintain records, not just for failing to file.

If documentation is missing, the IRS may disallow deductions entirely.

Compliance requires more than filing a form.

It requires structural awareness.

Recordkeeping Is Mandatory

Form 5472 compliance includes:

- Maintaining contemporaneous documentation

- Preserving related-party transaction records

- Supporting intercompany pricing and transfers

- Tracking ownership percentages annually

Failure to maintain proper records can independently trigger penalties.

If your firm is scaling foreign-owned clients or adding offshore bookkeeping support, structured systems like those outlined in Offshore Bookkeeping Workflow: Double Xero & QBO Systems become critical for defensible documentation.

A Proactive Compliance Framework

The safest approach is defensive and continuous.

Compliance Area | Strategic Control |

Ownership Monitoring | Confirm foreign ownership annually |

Transaction Ledger | Track every inflow and outflow involving foreign related parties |

Filing Calendar | Align Form 5472 with Form 1120 deadlines |

Mailing Controls | Confirm Ogden, UT submission for disregarded entities |

Record Retention | Maintain full transaction documentation |

Form 5472 cannot be handled reactively at year-end.

It requires structured year-round monitoring.

Expert Insight

“The $25,000 penalty is rarely about evasion. It is about structure. Foreign investors underestimate how technical U.S. reporting rules are. Once that misunderstanding compounds over multiple years, the exposure becomes significant.”

Shivangi Agrawal, Managing Director at SafeBooks Global

Strategic Takeaway for 2026

Section 6038A is not symbolic regulation.

It is an enforcement framework designed to ensure transparency in cross-border activity.

The penalty is automatic.

The defense is precision.

If your entity has foreign ownership and U.S. activity, proactive review is critical. Visit our Contact Us page to discuss structured compliance support before exposure escalates.