Trust account reconciliation is not just a monthly routine

Trust account reconciliation is one of the most important control processes for protecting client funds.

Even a small mismatch can signal a deeper issue.

Across regulated industries, nearly 38% of ethics violations are linked to trust account issues, and many firms face disciplinary action due to poor fund management.

Unlike standard bookkeeping, trust accounting deals with money that does not belong to the business. That changes everything.

Accuracy is no longer just about clean records. It is about compliance, accountability, and protecting client interests.

This is where structured systems like professional bookkeeping services play a critical role in maintaining consistency and audit readiness.

What is a trust account and why strict fund segregation matters

A trust account is used to hold money on behalf of clients. This could include retainers, escrow funds, deposits, or advance payments.

The key principle is simple:

Client funds must remain separate from business funds at all times.

This separation is not just best practice. It is enforced across industries and supported by structured accounting systems used by firms and businesses.

For firms handling multiple clients or properties, maintaining this separation becomes easier with organized workflows under accounting firm support systems.

There is a narrow exception where a small “float” may be maintained to cover bank charges. Beyond that, any mixing of funds becomes a compliance risk.

Why standard reconciliation is not enough for trust accounts

In normal bookkeeping, reconciliation compares bank balance with book balance.

That is a two-way check.

Trust accounts require clarity on ownership, not just totals. It is not enough to know how much money is in the account. You need to know who that money belongs to.

As firms scale and handle higher transaction volumes, relying on basic reconciliation increases risk. This is where structured service layers like backoffice support help maintain consistency across records.

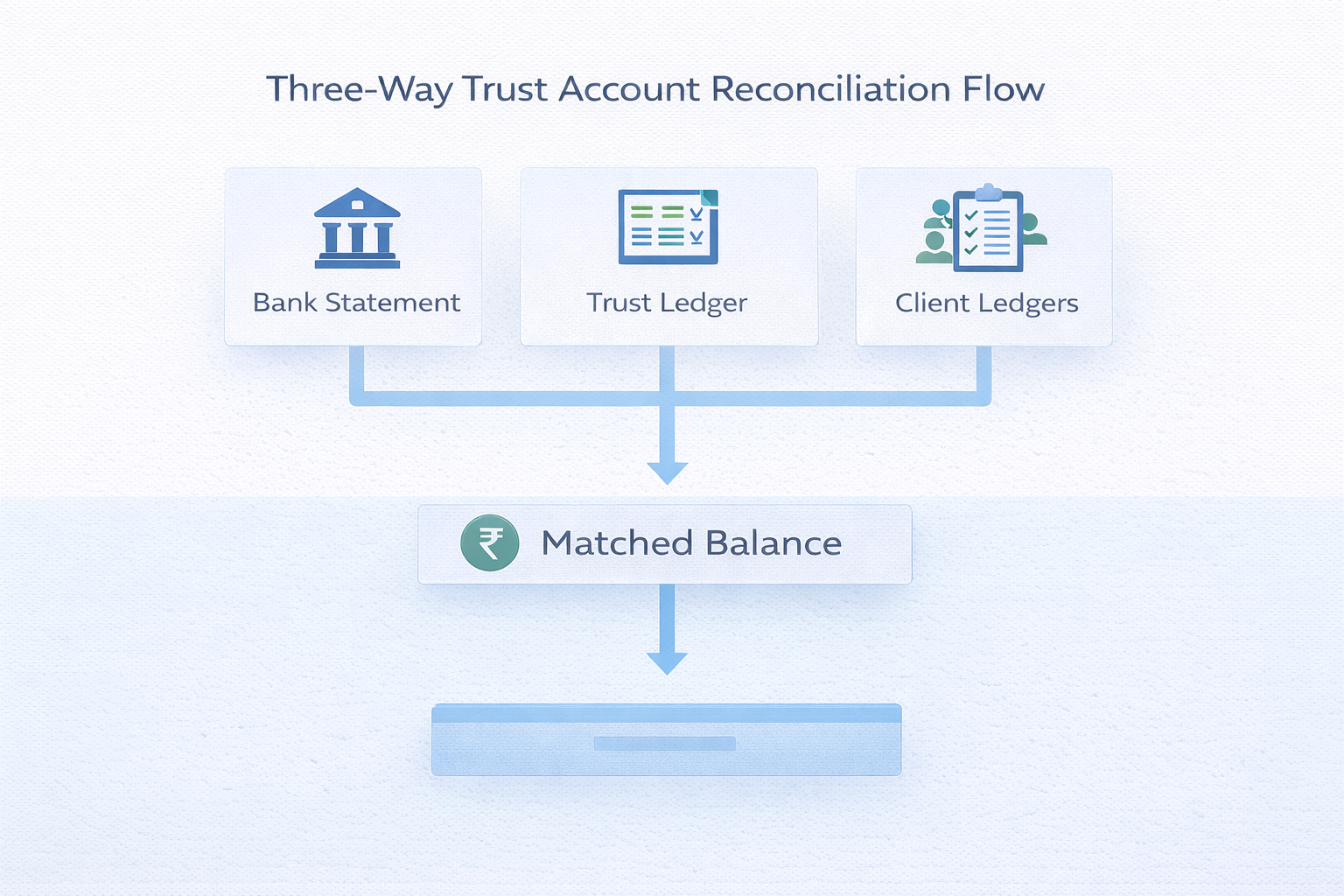

What is three-way trust account reconciliation and why it is required

Three-way reconciliation is the foundation of trust accounting.

It compares three independent records:

- Bank statement

- Trust ledger

- Client ledgers

The rule is strict:

All three must match exactly.

If they do not match, something is wrong.

There is no acceptable margin of error.

How monthly trust account reconciliation works step by step

A structured process keeps everything aligned.

The process begins with aligning all records. The bank statement, trust ledger, and client balances must reflect the same time period.

Next comes adjusting the bank balance. Deposits not yet reflected and checks not yet cleared must be accounted for.

This adjusted balance is then matched with the trust ledger.

After that, individual client balances are totaled.

The final verification is simple:

Bank balance = Trust ledger = Client total

Firms handling high transaction volumes often streamline this process through AR/AP software integration to reduce manual errors and improve accuracy.

Trust account reconciliation example table (three-way matching)

Component | Amount (₹) | Explanation |

Bank Ending Balance | 5,00,000 | As per bank statement |

+ Deposits in Transit | 50,000 | Not yet reflected |

– Outstanding Checks | 20,000 | Not yet cleared |

Adjusted Bank Balance | 5,30,000 | Actual position |

Trust Ledger Balance | 5,30,000 | Internal books |

Total Client Ledgers | 5,30,000 | Sum of balances |

Variance | 0 | Reconciliation complete |

Common trust account reconciliation mistakes that create compliance risk

Most issues build gradually.

Negative client balances are one of the most serious red flags. They indicate misuse of funds across accounts.

Commingling funds breaks the core rule of trust accounting.

Delayed reconciliation allows discrepancies to grow.

Stale checks must be reviewed and handled properly under compliance requirements.

As firms grow, these risks increase without structured oversight. Many firms address this by implementing layered processes through audit support services to maintain control and traceability.

Why monthly trust account reconciliation is critical for compliance

Trust account reconciliation is often mandatory.

Some jurisdictions require monthly checks, while others allow quarterly reconciliation. However, monthly reviews are widely expected.

In many cases, reconciliation must be reviewed, signed, and retained.

Compliance expectations continue to increase, especially for firms handling larger client bases.

Support functions such as tax support services help ensure consistency and reduce audit risk.

Why structured accounting systems improve reconciliation accuracy

Manual systems create gaps.

Structured systems reduce them.

With better workflows, firms can maintain consistent records, reduce reconciliation errors, and improve financial visibility.

You can see how process-driven accounting improves outcomes in real scenarios like CAS practice monthly close review support and CPA workflow automation.

Expert Insight

“Trust accounting is not just about balancing numbers, it is about maintaining accountability for funds that do not belong to the business. Even small gaps in reconciliation can lead to serious compliance risks. A structured three-way reconciliation process ensures accuracy, transparency, and audit readiness at all times.”

Bindesh Jain, Tax Director (CA, CS), SafeBooks

Why trust account errors lead to serious financial and regulatory consequences

Trust accounting errors do not stay internal.

They can lead to:

- disciplinary action

- license suspension

- financial penalties

- reputational damage

Regulators focus on control systems, not just intent.

Strong systems, supported by secure infrastructure and disciplined workflows, are essential.

What a properly maintained trust account looks like

A well-managed trust account always balances across all three records.

It clearly shows client-level balances and maintains complete documentation.

It is always audit-ready.

This level of clarity comes from consistency, not last-minute correction.

You can explore real outcomes through case studies or get started directly via Get Started.

If you prefer a direct conversation, reach out through Contact Us to set up a system that keeps your trust accounting accurate, compliant, and scalable.