BOI compliance is no longer a universal filing exercise.

After FinCEN’s 2025 interim final rule, most U.S.-created entities are exempt, while certain foreign entities registered to do business in the U.S. still face strict filing and update timelines. (FinCEN.gov)

For CPA firms, the 2026 playbook is simple:

- Classify clients correctly

- Communicate clearly

- Avoid collecting sensitive data through email

- Document boundaries to reduce professional liability risk

What changed in 2025 and why it matters in 2026

FinCEN’s interim final rule narrowed BOI reporting so the primary in-scope group is foreign entities registered to do business in a U.S. state or tribal jurisdiction.

That means most client confusion in 2026 comes from outdated assumptions like:

- “Every LLC must file BOI”

- “Domestic companies have to update BOI forever”

- “If we filed once, we are done”

None of those statements are safe to repeat without first confirming the entity type and registration status.

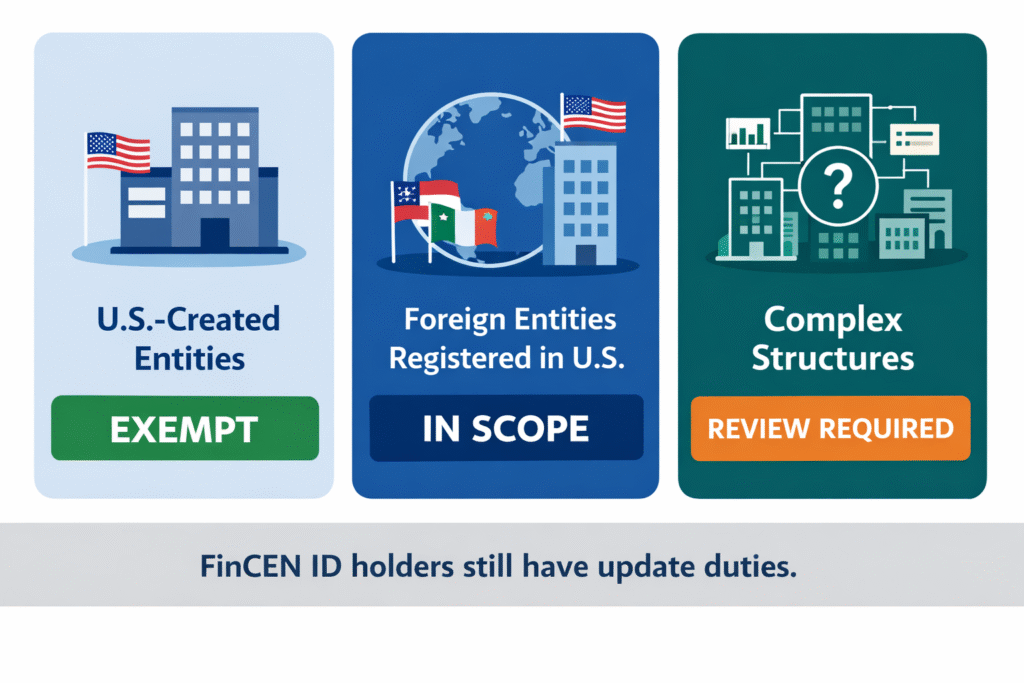

Who is in scope right now

The cleanest CPA workflow is to ask two questions first:

- Where was the entity formed?

- Is it registered to do business in any U.S. state?

Then categorize clients.

Client type | BOI status in 2026 | What the CPA firm should do |

Entity created in the U.S. | Typically exempt under the current rule | Inform client, document the basis, monitor for changes |

Foreign entity registered to do business in the U.S. | In scope unless an exemption applies | Confirm deadlines, build an update tracking process |

Multi-entity or cross-border structure | Needs fact check before guidance | Use a structured intake and confirm with legal counsel if needed |

The deadlines CPA firms should communicate

FinCEN’s timing rules generally require timely initial reporting and updates after changes.

Your client message should be:

- If you are in scope, you may have an initial filing deadline tied to registration notice.

- If anything changes in previously reported information, updates are generally due within 30 days.

Do not bury this in a long email. Put it in your onboarding workflow.

If you want a clean client process for collecting documents and approvals without inbox chaos, align BOI handling with your portal-based operating system, similar to the workflow in Remote accounting workflow setup.

The FinCEN ID trap CPAs must warn clients about

This is the part many firms are not saying clearly enough.

If a U.S. person obtained a FinCEN Identifier in 2024, they can still have a legal obligation to update the personal information tied to that identifier within 30 days of a change, such as a home address move or an ID renewal.

Key points to tell clients:

- A FinCEN ID is optional, but once obtained, updates are still required if information changes.

- There is currently no clear, official deactivation mechanism that removes the update obligation entirely. FinCEN has discussed assessing options, but clients should assume the update duty remains unless FinCEN issues a formal change. (Center for Agricultural Law and Taxation)

This is where email attachments become a liability. You are dealing with highly sensitive PII.

If your firm wants a client-facing explanation of why portals matter, point clients to How SafeBooks protects client financial data.

New York client update: NYLLCTA narrowed as of Jan 1, 2026

For firms with New York clients, the NYLLCTA update is a real operational detail.

As of January 1, 2026, the New York LLC Transparency Act took effect with a narrowed scope after a December 2025 veto, so it applies primarily to foreign LLCs authorized to do business in New York, mirroring the federal direction rather than expanding it. (Sidley Austin)

Client-friendly guidance:

- Domestic U.S.-formed LLCs are generally not the focus under the narrowed NYLLCTA scope.

- Foreign LLCs registering in New York should plan for additional reporting and deadline management.

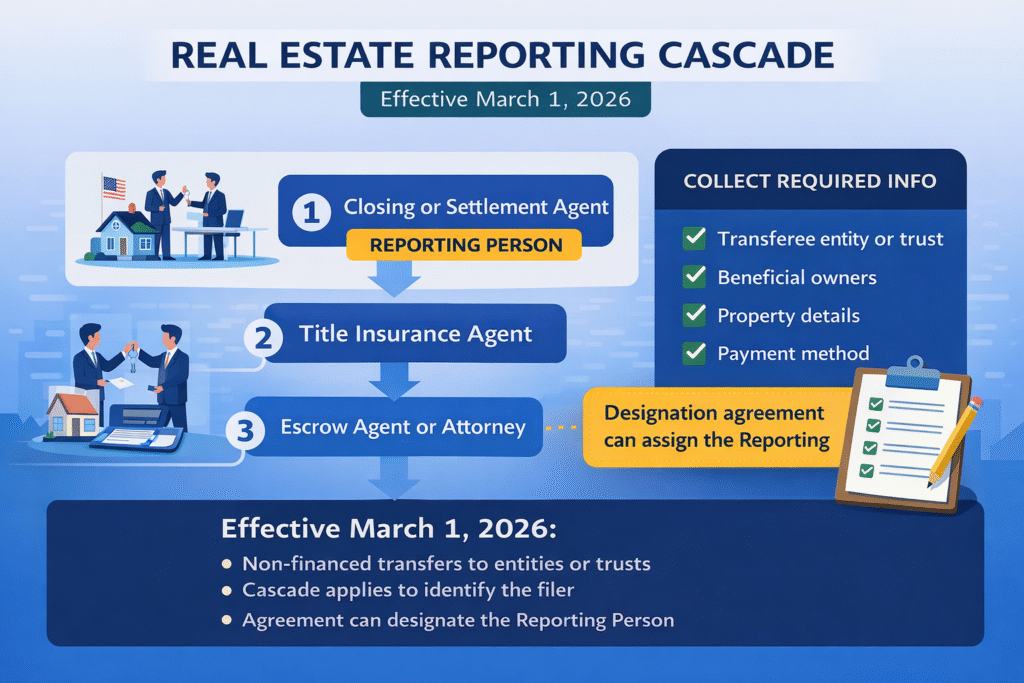

2026 curveball: real estate reporting and the reporting cascade

FinCEN’s residential real estate reporting framework matters because clients will ask their CPA first, even if the CPA is not the filing party.

FinCEN uses a “reporting cascade” to determine who the reporting person is, and importantly, parties involved can enter a written designation agreement to assign who will file the report, as long as the otherwise responsible party is part of that agreement.

Practical CPA value:

- Ask clients early: “Who is the designated reporting person for the closing?”

- Encourage clients to confirm this in writing during closing coordination so reporting does not fall through gaps.

Expert Insight

“BOI in 2026 is not about mass filing. It is about scope accuracy, secure data collection, and clear documentation of what the CPA firm did and did not take responsibility for.“

Shivangi Agrawal, Managing Director at SafeBooks Global

How SafeBooks supports CPA firms in this environment

If your firm supports foreign-owned clients, registrations across states, or complex entity structures, SafeBooks can help standardize your back-office workflows so nothing lives in scattered inbox threads.

Explore support options here:

If you want to review your current BOI client segmentation, update tracking, or documentation workflows, schedule a structured discussion through Contact Us.

In a regulatory environment that keeps shifting, the firms that win are the ones with clean systems and clear boundaries.