Client funds are not business funds. That is the foundation of trust accounting, and getting it wrong can lead to serious legal and financial consequences.

In industries like legal, real estate, and financial services, handling client money creates a fiduciary responsibility. This is not just accounting. It is a regulated system designed to protect funds that do not belong to the business.

What Trust Accounting Is

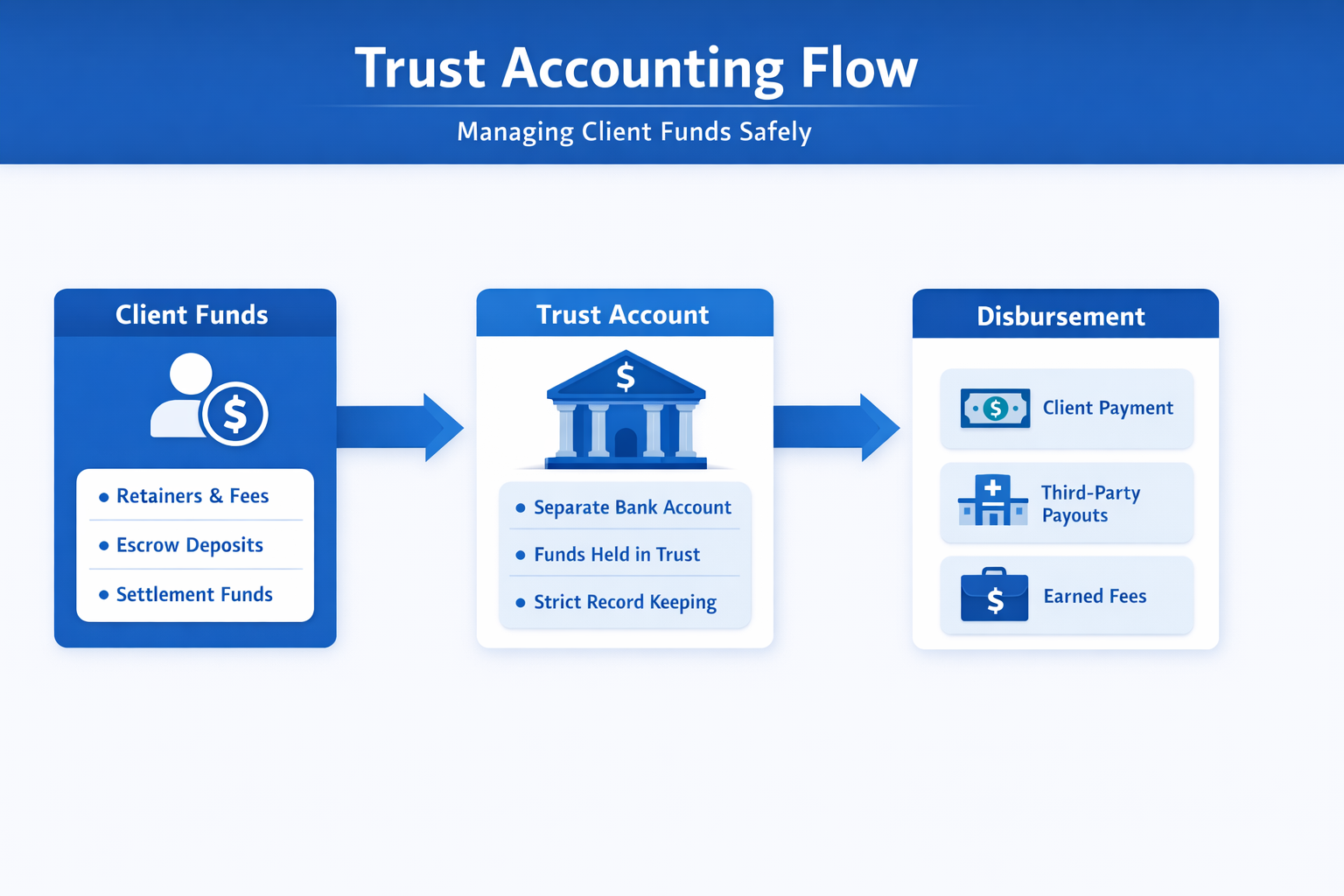

Trust accounting is the process of managing money held on behalf of clients or third parties.

These funds may include:

- Retainers or advance fees

- Settlement proceeds

- Escrow or earnest money

- Security deposits

From an accounting perspective, these funds are not income. They are recorded as liabilities because they must be returned or distributed based on defined conditions.

Why Client Funds Must Stay Separate

The most important rule in trust accounting is complete separation of funds.

Client funds must never be mixed with:

- Business operating accounts

- Personal funds

- Other client balances without proper tracking

This separation ensures:

- Transparency

- Regulatory compliance

- Protection of client money

- Clear audit trails

Even temporary use of client funds is treated as a serious violation.

Segregation Rules and Fiduciary Responsibility

Handling client funds creates a fiduciary obligation that goes beyond normal business conduct.

Core responsibilities include:

Loyalty

Client funds must never be used for business benefit, even for short-term cash flow.

Care

Funds must be handled with proper systems, timely recording, and secure banking practices.

Disclosure

Clients must be able to receive a clear and accurate statement of their funds at any time.

Failure to meet these responsibilities can lead to regulatory action, financial penalties, and reputational damage.

Common Trust Account Structures

Trust accounts are structured based on the type and duration of funds held.

IOLTA Accounts

Used for small or short-term funds. Interest is typically directed to public or legal aid programs.

Individual Trust Accounts

Used when funds are significant or held long enough to generate meaningful interest for the client.

Escrow Accounts

Used in structured transactions such as real estate, where funds are held until conditions are fulfilled.

Selecting the correct structure is essential for compliance and accurate reporting.

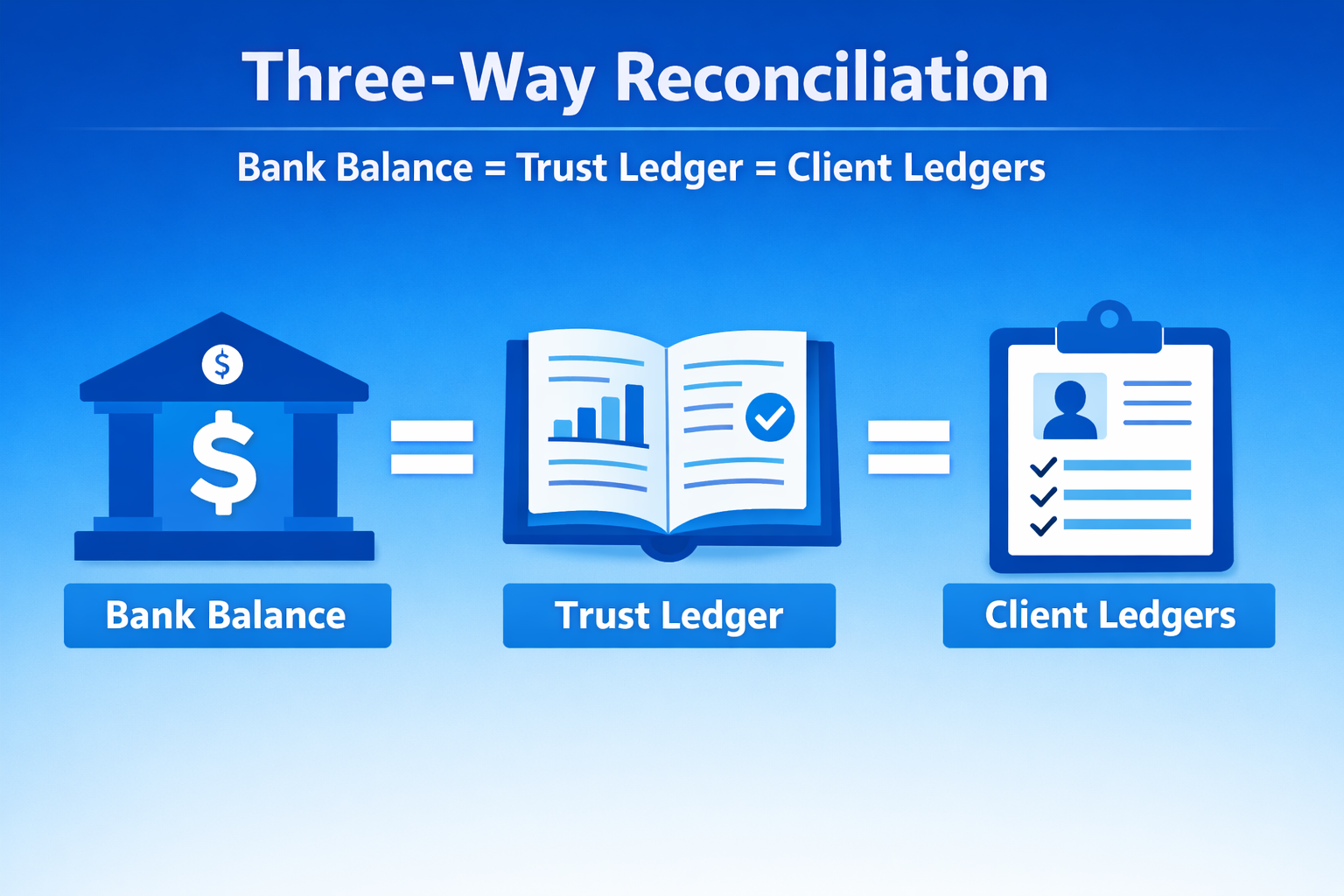

Why Reconciliation Is Required

Trust accounting requires stricter validation than standard accounting.

The Three-Way Reconciliation

This process ensures alignment between:

- Bank balance

- Internal trust ledger

- Total of individual client balances

Formula:

Bank Balance = Internal Ledger = Sum of Client Ledgers

This ensures that:

- Every dollar is accounted for

- No client funds are misallocated

- Errors are identified early

Modern systems like a continuous close accounting workflow help automate this process and reduce risk.

Cleared vs Collected Funds (Critical Distinction)

A common mistake in trust accounting is assuming funds are safe to use once they appear in the bank.

In reality:

- Cleared funds appear in your account

- Collected funds are fully transferred from the payer’s bank

This process can take 3 to 10 business days.

Disbursing funds before they are collected can result in:

- Accidental use of other clients’ money

- Trust account shortages

- Compliance violations

This is one of the most common causes of unintentional trust breaches.

The TAON Rule and Regulatory Oversight

Trust accounts operate under strict regulatory surveillance.

Under Trust Account Overdraft Notification (TAON) rules, banks in over 40 jurisdictions are required to report any trust account overdraft to regulatory authorities immediately.

This applies even if:

- The overdraft was caused by a bank error

- The bank temporarily covers the shortfall

Once reported, it can trigger:

- Regulatory review

- Audit requests

- Investigation into account practices

This makes even minor mistakes highly visible and risky.

Common Mistakes in Trust Accounting

Common issues include:

- Mixing client and business funds

- Using trust funds temporarily

- Delayed reconciliation

- Incorrect client allocation

- Disbursing funds before collection

These mistakes often begin as operational gaps but can escalate into serious violations.

Record Retention Requirements

Trust accounting requires maintaining a complete audit trail.

Most regulatory bodies require records to be retained for 5 to 7 years after the matter is closed.

Required records typically include:

- Bank statements

- Client ledgers

- Reconciliation reports

- Transaction records

- Supporting documents and approvals

Incomplete records can lead to audit failures and compliance issues.

Risks of Treating Trust Funds Casually

Trust accounting violations carry serious consequences.

Regulatory Risks

- Audits triggered by overdrafts

- Mandatory reporting under TAON

- License suspension or revocation

Financial Risks

- Personal liability for fund misuse

- Insurance claim denial

- Increased compliance costs

Reputation Risks

- Loss of client trust

- Reduced business opportunities

- Long-term brand damage

Best Practices for Managing Trust Accounts

Area | Best Practice |

Fund Separation | Maintain strict segregation of client funds |

Recording | Track transactions at individual client level |

Reconciliation | Perform monthly three-way reconciliation |

Controls | Implement dual approvals for disbursement |

Timing | Use funds only after they are fully collected |

Documentation | Maintain records for 5 to 7 years |

Structured systems like professional bookkeeping services help enforce these practices consistently.

Expert Insight

“Most trust accounting issues are not intentional. They happen due to lack of systems. Once proper controls and reconciliation are in place, compliance becomes much easier to maintain.“

Shivangi Agrawal, Managing Director (CA, CPA USA), SafeBooks

How SafeBooks Supports Trust Accounting

Managing trust accounts requires structured processes and regulatory awareness.

SafeBooks helps firms:

- Maintain proper fund segregation

- Implement compliant trust accounting systems

- Perform accurate reconciliation

- Prepare audit-ready records

Explore solutions through back office accounting support. Trust accounting is not just a process. It is a responsibility tied to professional integrity.

Strict segregation, timely reconciliation, and proper systems ensure that client funds remain protected and compliant. Organizations that follow these practices reduce risk and build long-term trust.

If your current setup lacks structure, it may be time to strengthen your systems. You can connect through the SafeBooks contact page to evaluate your approach.