Why 2026 Changes Capital Expenditure Planning Entirely

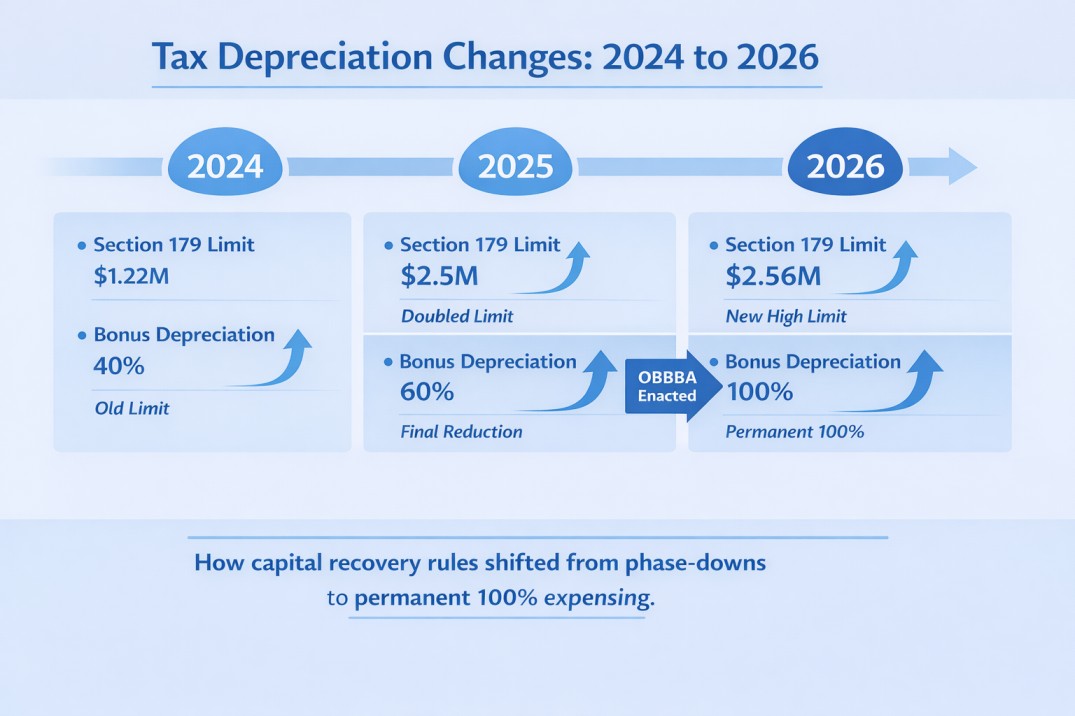

The 2026 tax year represents a structural reset in how US businesses recover capital costs. After years of temporary extensions and scheduled phase-downs, the One Big Beautiful Bill Act permanently reshaped depreciation planning.

Two changes define this shift:

- Section 179 expensing limits have effectively doubled, reaching an inflation-adjusted cap of approximately $2.56 million in 2026.

- 100% bonus depreciation has been permanently restored for qualifying property acquired and placed in service after January 19, 2025.

The result is not simply larger deductions. It is precision.

Businesses that continue to expense everything automatically risk mismanaging taxable income tiers, interest deductibility under Section 163(j), AMT exposure, and state-level tax outcomes. In 2026, depreciation planning becomes a surgical exercise rather than a one-size-fits-all decision.

Understanding Section 179 in 2026

Section 179 remains the most precise depreciation tool available to small and mid-sized businesses because it allows taxpayers to determine exactly how much cost is recovered in the current year.

Section 179 Limits and Phase-Out for 2026

Parameter | 2026 Amount |

Maximum Section 179 deduction | $2,560,000 |

Phase-out begins at | $4,090,000 |

Deduction fully eliminated at | $6,650,000 |

Once total qualifying purchases exceed the phase-out threshold, the deduction is reduced dollar for dollar. This design intentionally targets Section 179 toward controlled income management rather than unlimited expensing.

Income Limitation as a Strategic Lever

Section 179 cannot create or increase a net operating loss. The deduction is limited to taxable income from the active conduct of trade or business.

Any unused Section 179 carries forward indefinitely.

This limitation is what makes Section 179 valuable. It allows businesses to reduce taxable income to a defined target without overshooting into low-value brackets or unintended losses. Firms using tax support services for accounting firms frequently rely on Section 179 as the final income calibration step.

The Permanent Return of 100% Bonus Depreciation

Section 168(k) bonus depreciation is permanently restored to 100% for qualifying property acquired and placed in service after January 19, 2025.

This eliminates the prior phase-down schedule and removes artificial pressure to accelerate purchases based on expiring incentives.

Bonus Depreciation Characteristics

Feature | 2026 Rule |

Bonus percentage | 100% |

Used property eligibility | Allowed if new to taxpayer |

Income limitation | None |

Can create NOL | Yes |

Election out | By asset class |

Bonus depreciation is volume-oriented. It is most effective when the objective is maximum immediate write-off and cash-flow acceleration, even if that creates a loss.

Expert Insight

“In 2026, the most common planning error is treating full expensing as automatic. Section 179 and bonus depreciation affect interest limits, AMT exposure, and state taxes very differently. The real value comes from sequencing them intentionally.”

Bindesh Jain, Tax Director (CA, CS), SafeBooks

Why Mixing Section 179 and Bonus Depreciation Matters

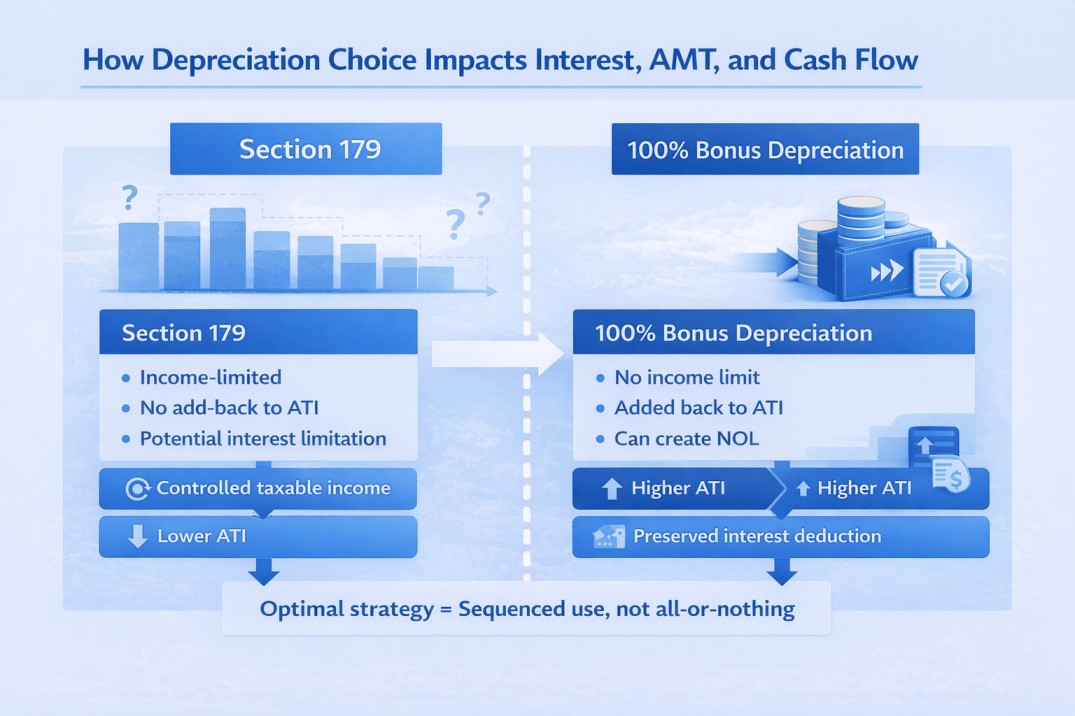

Section 163(j) Interest Deduction Impact

Business interest deductions are limited to 30% of Adjusted Taxable Income (ATI) under Section 163(j).

OBBBA restored the EBITDA-based ATI calculation, allowing depreciation to be added back. However, the treatment differs:

- Bonus depreciation is added back to ATI

- Section 179 is not added back

This distinction directly affects interest capacity.

Interest Deduction Comparison

Variable | 100% Bonus | Section 179 |

Depreciation add-back to ATI | Yes | No |

Resulting ATI | Higher | Lower |

Allowable interest deduction | Higher | Lower |

For leveraged businesses, excessive use of Section 179 can unintentionally restrict interest deductions, creating carryforwards and liquidity pressure. This issue commonly surfaces during audit and technical review engagements.

The Section 168(n) “Super-Deduction” for Manufacturers

One of the most consequential but often overlooked changes under OBBBA is Section 168(n), which introduces a 100% depreciation allowance for Qualified Production Property (QPP).

Historically, nonresidential real property such as factories and refineries was depreciated over 39 years. Section 168(n) allows qualifying portions of these facilities to be fully expensed in year one.

Substantial Transformation Requirement

To qualify, the facility must be used in manufacturing, refining, agricultural production, or chemical production that results in a substantial transformation of tangible property.

Activities that do not qualify include:

Excluded Area | Reason |

Administrative offices | Not integral to production |

Warehousing and storage | Post-production activity |

Showrooms and sales floors | Commercial use |

Packaging or minor assembly | No substantial transformation |

R&D laboratories | Governed by Section 174 |

Only the portion of the building directly tied to production qualifies, making cost segregation studies essential in 2026.

Recapture Guardrail

Section 168(n) includes a 10-year recapture rule.

If the facility ceases to be used for qualified production within ten years of being placed in service, the previously deducted amount is recaptured as ordinary income in the year of change. This rule requires long-term operational planning, especially for facilities that may shift from manufacturing to distribution.

Surgical Income Planning for Pass-Through Entities

For pass-through owners, depreciation strategy should align with marginal tax brackets, not total deductions.

Targeted expensing can eliminate income taxed at 35% or 37% while preserving deductions for future high-income years. Section 179 income limitations and bonus depreciation opt-out elections make this precision possible.

This modeling approach is increasingly used in engagements supported by bookkeeping and accounting teams.

AMT Exposure Requires Advanced Modeling

While higher AMT exemptions remain permanent, the phase-out threshold has been lowered and the phase-out rate increased.

Large depreciation deductions can accelerate AMT exposure by eroding exemptions faster than expected. Without modeling, deductions intended to reduce tax may be partially neutralized.

State Tax Conformity Alters Real Savings

Federal depreciation benefits do not guarantee state-level relief.

State | Bonus Depreciation | Section 179 |

California | Decoupled | $25,000 cap |

Michigan | Partial decoupling | Pre-OBBBA limits |

Maine | Selective conformity | Conforms |

Kansas | Static conformity | Decoupled |

In nonconforming states, federal savings may be offset by higher current-year state taxes. Cost segregation remains valuable because many states still respect accelerated asset lives.

Capital Budgeting Implications for CFOs

Permanent 100% expensing materially improves first-year cash flow, lowers effective after-tax investment cost, and increases project net present value.

With bonus depreciation no longer expiring, capital timing decisions should be driven by operational readiness rather than tax deadlines, except where temporary provisions like Section 168(n) apply.

The 2026 Depreciation Planning Imperative

The 2026 tax environment does not reward aggressive expensing. It rewards sequencing, modeling, and intent.

Section 179, 100% bonus depreciation, and the new Section 168(n) super-deduction are not competing tools. Used correctly, they allow businesses to manage taxable income tiers, preserve interest deductibility, mitigate AMT exposure, and align tax outcomes with long-term financial strategy.

SafeBooks supports accounting firms and businesses with depreciation modeling, multi-year tax planning, and defensible documentation across complex capital structures.

To discuss how SafeBooks can support capital expenditure planning and depreciation strategy execution, contact us to speak with our team.