A nonprofit board should not wait for year-end to understand the numbers. Monthly reporting gives leadership the clarity needed to govern responsibly.

When boards rely only on annual reports, they react too late. Monthly visibility helps identify risks early, improve decision-making, and ensure funds are used correctly.

Why Boards Need Monthly Financial Visibility

Nonprofits operate in a dynamic environment where funding, expenses, and program needs change frequently.

Monthly reporting helps boards:

- Identify financial risks early

- Track whether funds are being used as intended

- Make timely strategic decisions

- Maintain compliance and donor trust

Without regular reporting, boards operate without real visibility, which increases the risk of financial mismanagement.

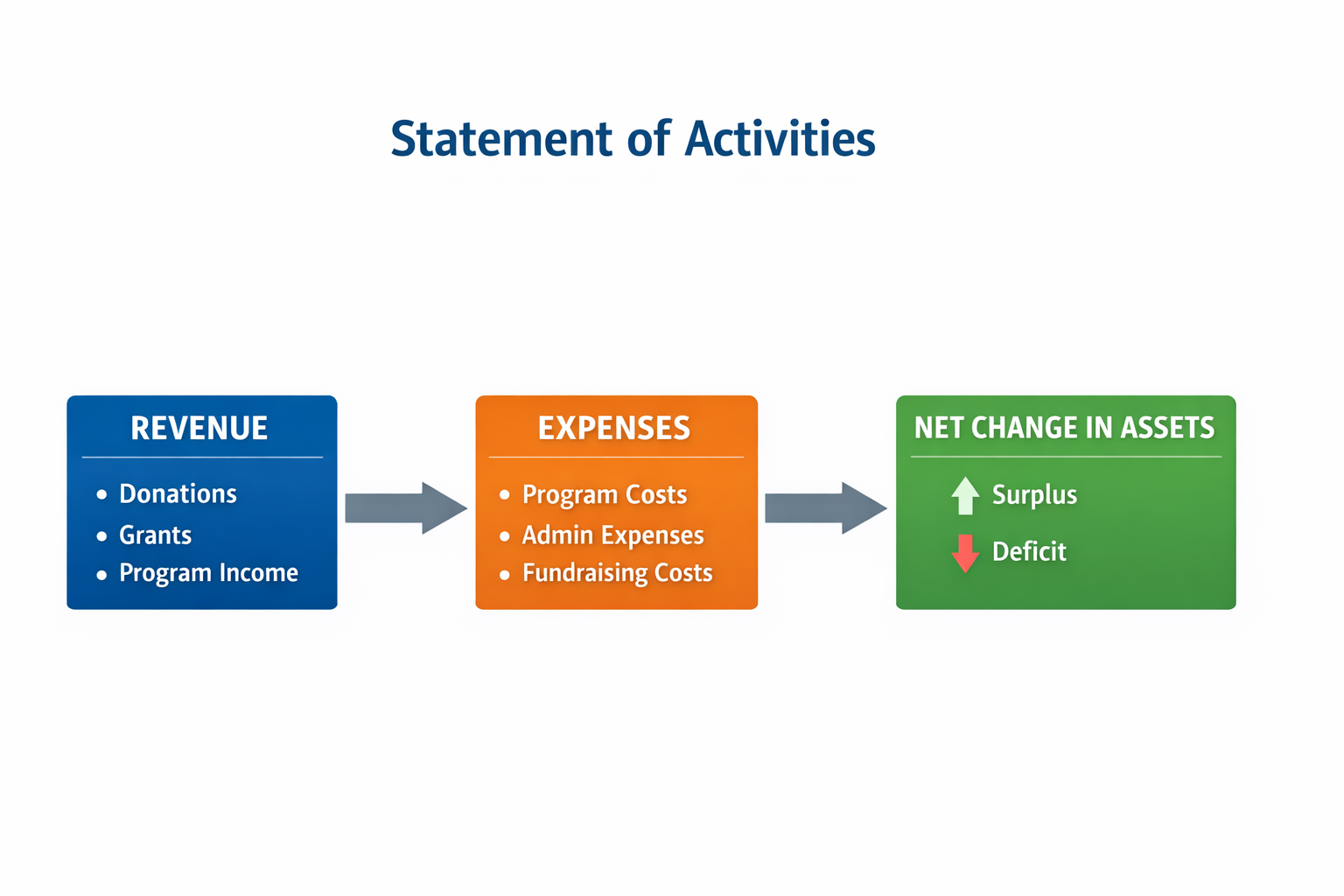

Statement of Activities Explained

The Statement of Activities is similar to an income statement. It shows how much revenue the nonprofit earned and how much it spent over a specific period.

It answers a simple question:

Are we financially sustainable?

Key components include:

- Revenue (donations, grants, program income)

- Expenses (program, administrative, fundraising)

- Change in net assets

What board members should look for:

- Are expenses growing faster than revenue?

- Is there consistent deficit spending?

- Is revenue dependent on a single source?

Statement of Financial Position Explained

The Statement of Financial Position is the nonprofit equivalent of a balance sheet. It shows what the organization owns and owes at a specific point in time.

It answers:

Are we financially stable right now?

It includes:

- Assets (cash, receivables, equipment)

- Liabilities (payables, obligations)

- Net assets (restricted and unrestricted funds)

What board members should look for:

- Does the organization have enough cash to operate?

- Are liabilities increasing faster than assets?

- How much of the funds are actually usable (unrestricted)?

Statement of Functional Expenses (Often Overlooked)

This is one of the most important yet often ignored reports in nonprofit accounting.

The Statement of Functional Expenses is mandatory for 501(c)(3) organizations. It breaks down expenses in two ways:

- By function: program, administrative, fundraising

- By nature: salaries, rent, utilities, etc.

Why it matters:

- Shows how efficiently funds are used

- Helps validate program spending ratios

- Ensures transparency for donors and regulators

Boards should review this to confirm that expenses are correctly allocated and not misclassified.

Budget vs Actual Reporting

Budgets represent plans. Actuals show reality.

The Budget vs Actual report compares expected numbers with real performance.

Area | What to Check | Why It Matters |

Revenue | Is actual income below target? | Indicates funding risk |

Expenses | Are costs higher than planned? | Signals overspending |

Variance | Are differences significant? | Requires explanation |

Trends | Are patterns consistent? | Helps forecast future |

Expert practice:

Many boards define a threshold for significance, such as:

- Variance greater than 10%

- Or variance above $5,000

Any variance beyond this should require a written explanation.

Organizations using structured systems like a continuous close accounting workflow can monitor these deviations in real time instead of reacting late.

Cash Flow and Liquidity Review

Profit does not always mean cash availability.

A nonprofit may show strong financials but still struggle to pay expenses due to timing gaps in funding.

Boards must review:

- Cash inflows vs outflows

- Available operating cash

- Restricted vs unrestricted cash

Understanding Spendable Wealth (LUNA)

A more accurate measure than cash is Liquid Unrestricted Net Assets (LUNA).

LUNA = Unrestricted funds minus non-liquid assets like property and equipment

Why it matters:

- Shows funds actually available for operations

- Avoids overestimating financial strength

- Helps assess sustainability

Healthy nonprofits typically maintain 3 to 6 months of LUNA as a safety buffer.

What Board Members Should Look For Each Month

Monthly reports are not just for review. They are for action.

Board members should actively look for:

- Declining or unstable revenue trends

- Increasing expenses without clear justification

- Delays in financial reporting

- Low or shrinking cash reserves

- Overdependence on a single funding source

Critical Red Flags

Some indicators require immediate attention:

- Unreconciled bank accounts

- Growing payroll tax liabilities (serious legal risk)

- Frequent use of restricted funds for operations

- High turnover in finance roles

- Inconsistent or unclear reporting

These are not minor issues. They often signal deeper financial control problems.

Strong systems supported through nonprofit bookkeeping services help identify and resolve these risks early.

Expert Insight

“Boards should not just review reports. They should question them. The quality of financial oversight directly impacts the organization’s long-term sustainability.“

Shivangi Agrawal, Managing Director (CA, CPA USA), SafeBooks

How SafeBooks Supports Nonprofit Financial Reporting

Nonprofits need clear, structured, and timely financial reporting to support governance.

SafeBooks helps organizations:

- Prepare accurate monthly financial reports

- Track restricted and unrestricted funds

- Build board-ready reporting formats

- Improve visibility across financial data

Explore solutions for back office accounting support. Strong governance depends on clear financial visibility. Monthly reporting allows boards to move from reactive decisions to proactive leadership.

Nonprofits that consistently review financial reports are better equipped to manage risks, maintain trust, and sustain long-term impact.

If your organization lacks structured reporting, it may be time to improve your financial systems. You can connect through the SafeBooks contact page to get started.