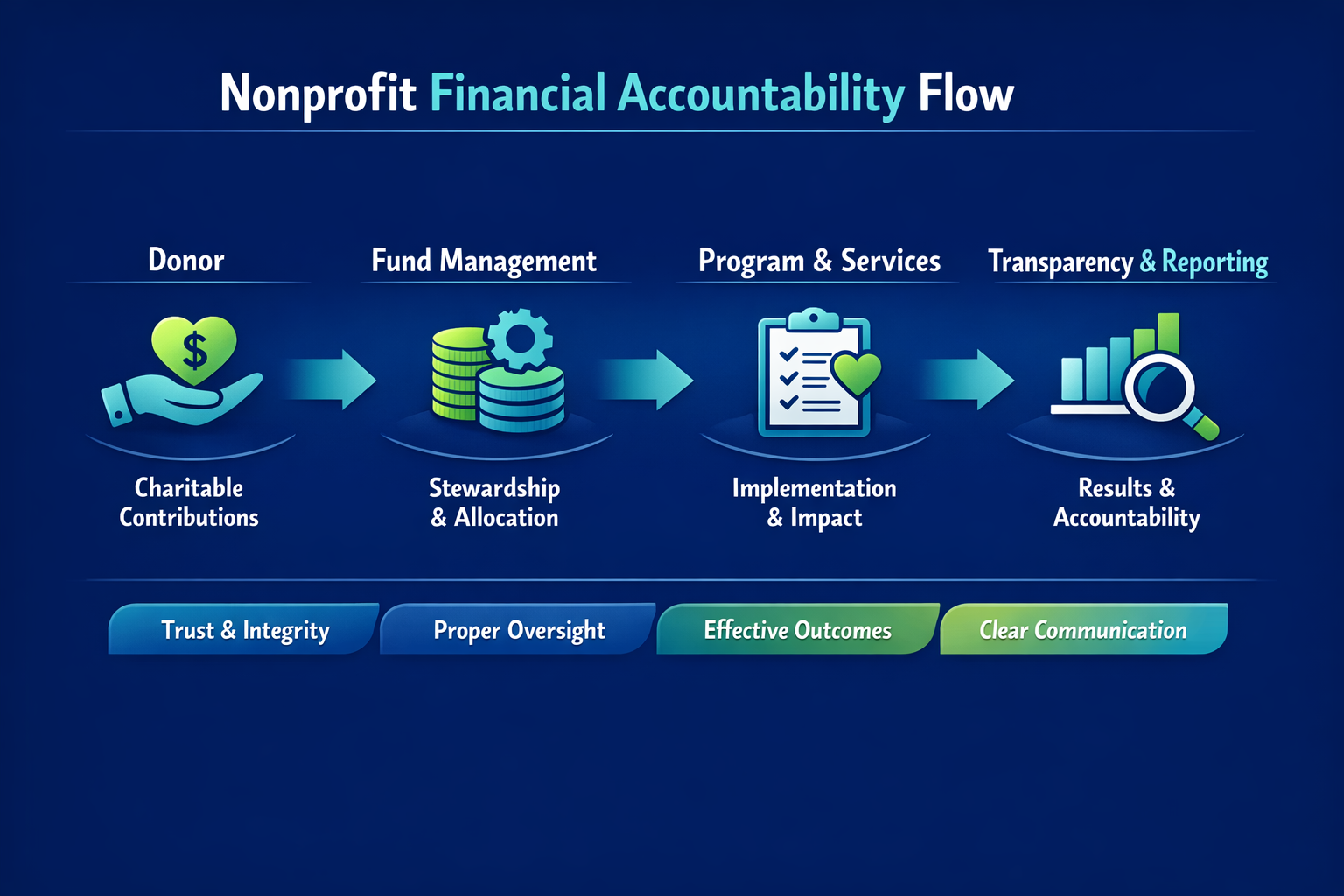

Strong missions still need strong accounting. When nonprofits make financial mistakes, the impact goes beyond numbers. It affects trust, compliance, and funding.

Many nonprofits operate with good intent but weak financial systems. Over time, small accounting errors turn into serious risks that affect audits, donor confidence, and long-term sustainability.

Why Accounting Discipline Matters in Nonprofits

Nonprofits are built on accountability. Every dollar received is tied to a purpose, and every expense must be justified.

Unlike businesses, nonprofits are judged by how responsibly they use funds, not by profit.

Weak accounting is not just an internal issue. It has real consequences:

- Loss of donor trust

- Audit failures

- Grant rejection

- Legal and regulatory risks

A critical example: The IRS has automatically revoked tax-exempt status for over 440,000 organizations due to failure to file required returns.

This makes one thing clear. Accounting is not a back-office function. It is core to survival.

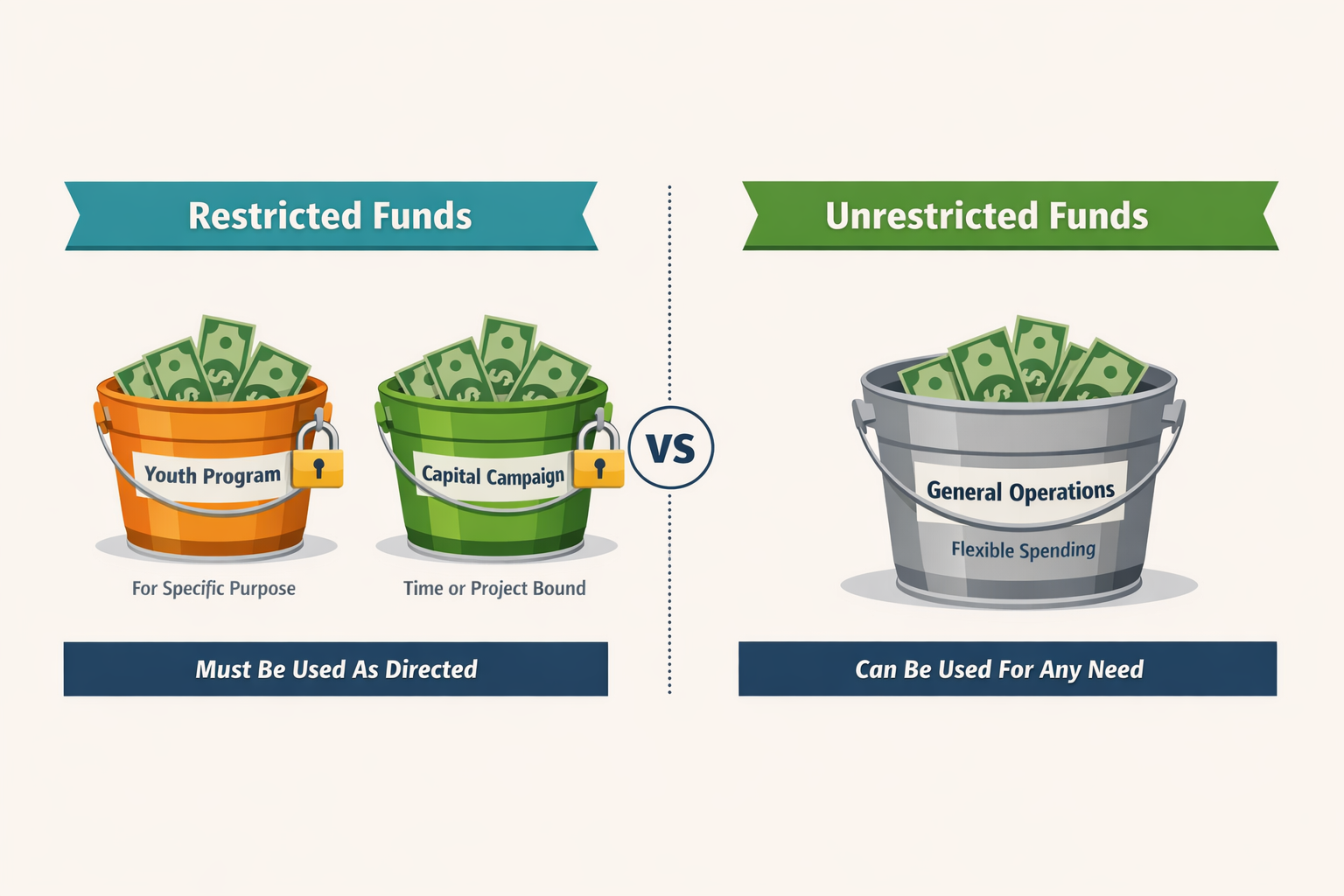

Mixing Grant Funds and Restricted Money

One of the most common and serious mistakes is mixing restricted and unrestricted funds.

Restricted funds must be used exactly as specified by donors. Unrestricted funds are meant for general operations.

Common issues include:

- Using grant funds for operational expenses

- Covering short-term cash gaps with restricted money

- Failing to track fund usage separately

Even temporary misuse can lead to compliance violations and reputational damage.

Poor Documentation and Weak Audit Trails

Documentation is the foundation of financial credibility. Without it, transactions cannot be validated.

Common issues include:

- Missing invoices or receipts

- No grant agreements on record

- Lack of expense justification

- Disorganized or manual record keeping

This becomes a major problem during audits. Unsupported expenses can be disallowed, forcing nonprofits to return funds.

Strong systems, such as those built through financial data protection frameworks, ensure every transaction is backed and traceable.

Lack of Regular Board Reporting

Financial oversight depends on visibility. Many nonprofits fail to provide consistent and meaningful reports to their boards.

Key issues include:

- Delayed reporting

- Overly complex or unclear data

- No budget vs actual tracking

- Lack of discussion around financial risks

Boards should regularly review:

- Financial position

- Income and expenses

- Cash flow

- Budget performance

Without this, decision-making becomes reactive instead of strategic.

Weak Internal Controls and Approval Processes

Internal controls protect nonprofits from both error and fraud.

Many organizations operate with limited staff, which often leads to overlapping roles. This creates serious risk.

Common gaps include:

- One person handling multiple financial responsibilities

- No approval workflows

- No payment authorization checks

- Weak payroll oversight

Industry data shows that organizations lose around 5% of annual revenue to fraud, and nearly 30% of cases occur due to lack of segregation of duties.

Practical control improvements:

- Separate responsibilities for recording, approving, and reconciling

- Require dual approval for payments

- Implement dual signatures for checks above $1,000

- Set clear spending limits and authorization levels

How Nonprofits Can Strengthen Financial Oversight

Improvement does not require complexity. It requires discipline and structured systems.

Here is a simple comparison:

Area | Common Mistake | Better Approach |

Fund Tracking | Mixing restricted and unrestricted funds | Separate fund tracking with clear allocation |

Documentation | Missing or unorganized records | Centralized and structured document storage |

Reporting | Delayed or unclear reports | Monthly reporting with budget comparison |

Controls | One person handling all tasks | Segregation of duties and approval workflows |

Payments | No authorization checks | Dual approval and threshold-based controls |

Organizations moving toward structured systems, such as a continuous close accounting workflow, are also adopting 2026 trends like continuous close, where transactions are reconciled in real time instead of relying on month-end processes.

Expert Insight

“Most nonprofit accounting issues begin with small gaps in tracking and approvals. Over time, these gaps turn into risks. Strong systems help prevent problems before they grow.“

Bindesh Jain, Tax Director (CA, CS), SafeBooks

How SafeBooks Supports Nonprofit Financial Management

Nonprofits need structured financial systems that support compliance and transparency.

SafeBooks helps organizations:

- Track restricted and unrestricted funds accurately

- Maintain audit-ready documentation

- Improve financial reporting for boards

- Build strong approval and control systems

Explore solutions for nonprofit bookkeeping services and scalable support through back office

Small accounting mistakes can create serious risks if ignored. Organizations that build strong financial systems earn trust, maintain compliance, and secure long-term funding.

If your organization is facing challenges with tracking, reporting, or controls, it may be time to strengthen your financial systems. You can connect through the SafeBooks contact page to evaluate your current setup.