Your POS shows one number. Your bank shows another.

That does not always mean something is wrong. But it does mean you are looking at two different versions of the same transaction.

In modern restaurants, money does not move in a straight line. It moves through processors, platforms, batching cycles, and settlement delays before it reaches your bank.

This gap between sales and deposits is not an error. It is a structural reality of how restaurant finance works today.

Understanding it is the difference between guessing your numbers and actually controlling them.

Why Restaurant Sales and Deposits Often Differ

Restaurant sales reports reflect what happened operationally.

Bank deposits reflect what actually settled financially.

These are not the same moment.

Common causes of differences include:

- Timing delays between transaction and settlement

- Payment processor fees deducted before payout

- Refunds and chargebacks

- Third-party delivery commissions

- Tips and tax handling

- Batch cutoffs and banking schedules

At any given time, part of your revenue is in transit. It has been recorded in the POS but has not yet reached your bank.

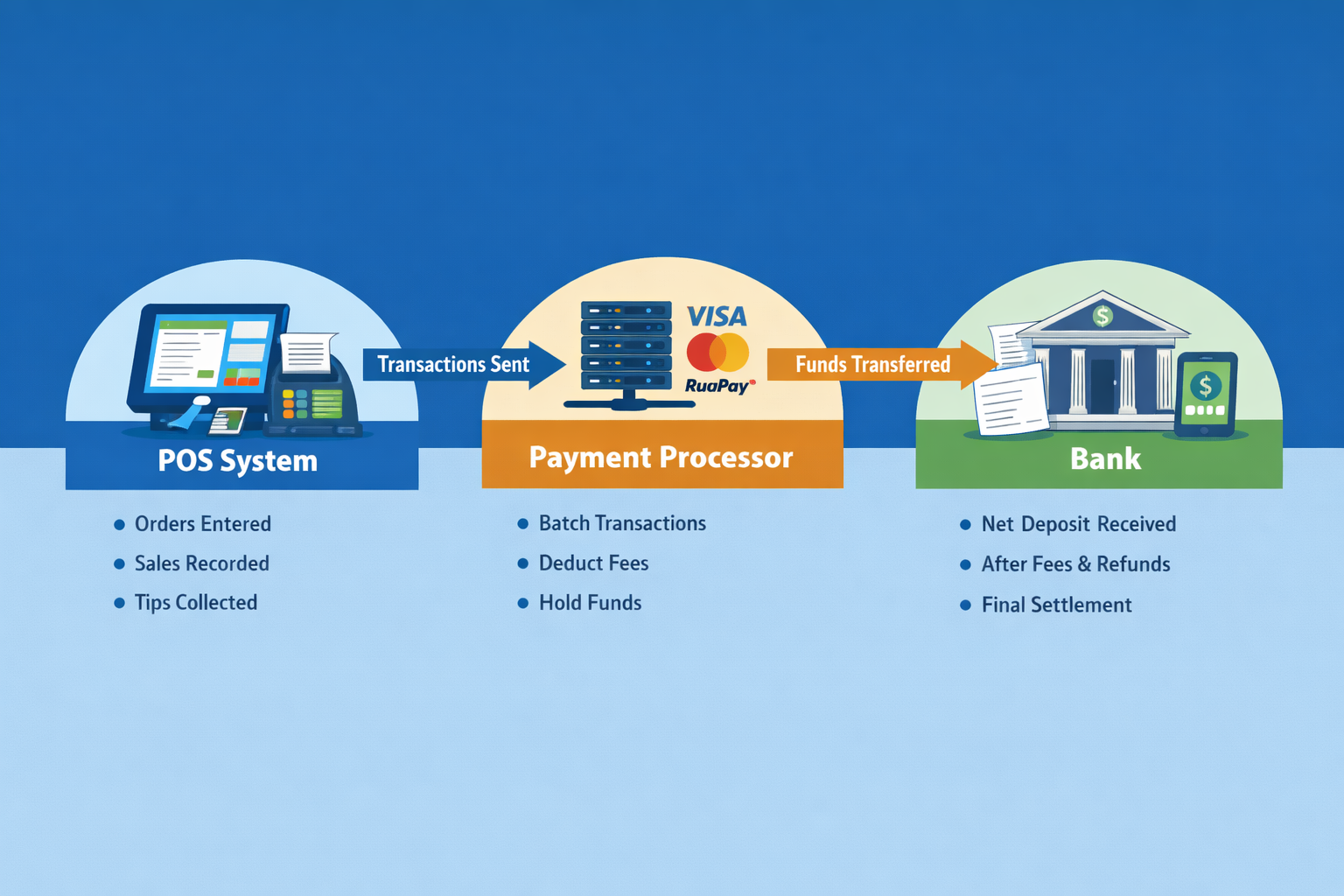

How POS Systems Record Sales vs How Banks Receive Funds

A POS system records sales instantly.

The moment an order is closed, it logs:

- Total sale amount

- Taxes collected

- Payment method

- Tips

This is called order-day reporting.

Banks operate differently. They only record funds once the transfer is completed. This is settlement-day reporting.

That means:

- A Friday sale may hit the bank on Monday

- Late-night sales may fall into the next day’s batch

- Weekend transactions may be delayed

This creates a natural mismatch even when everything is working correctly.

Payment Processor Delays and Batching

Between your POS and your bank sits the payment processor.

Processors such as Stripe, Square, Clover, or Toast:

- Group transactions into batches

- Apply cutoff times

- Transfer funds after clearing

If your restaurant operates beyond the processor cutoff time, one day’s sales can be split across multiple deposits.

In addition, most processors follow a net settlement model, meaning they deduct fees before transferring funds.

For example:

- POS shows ₹100,000 in sales

- Processor deducts fees

- Bank receives ₹96,500

Without proper accounting, that difference looks like missing money.

Restaurants that standardize workflows using structured systems similar to the remote accounting workflow setup guide avoid this confusion by aligning transaction timing with accounting entries.

Credit Card Settlements, Tips, Refunds, and Fees

Card-based transactions introduce multiple adjustments before funds reach your account.

Processing Fees

Every card transaction includes:

- Merchant fees

- Gateway charges

- Platform deductions

These are removed before the deposit arrives.

Tips

Tips collected via cards are not revenue. They are a liability owed to staff.

If tips are paid out in cash or through payroll, they affect your deposit amount.

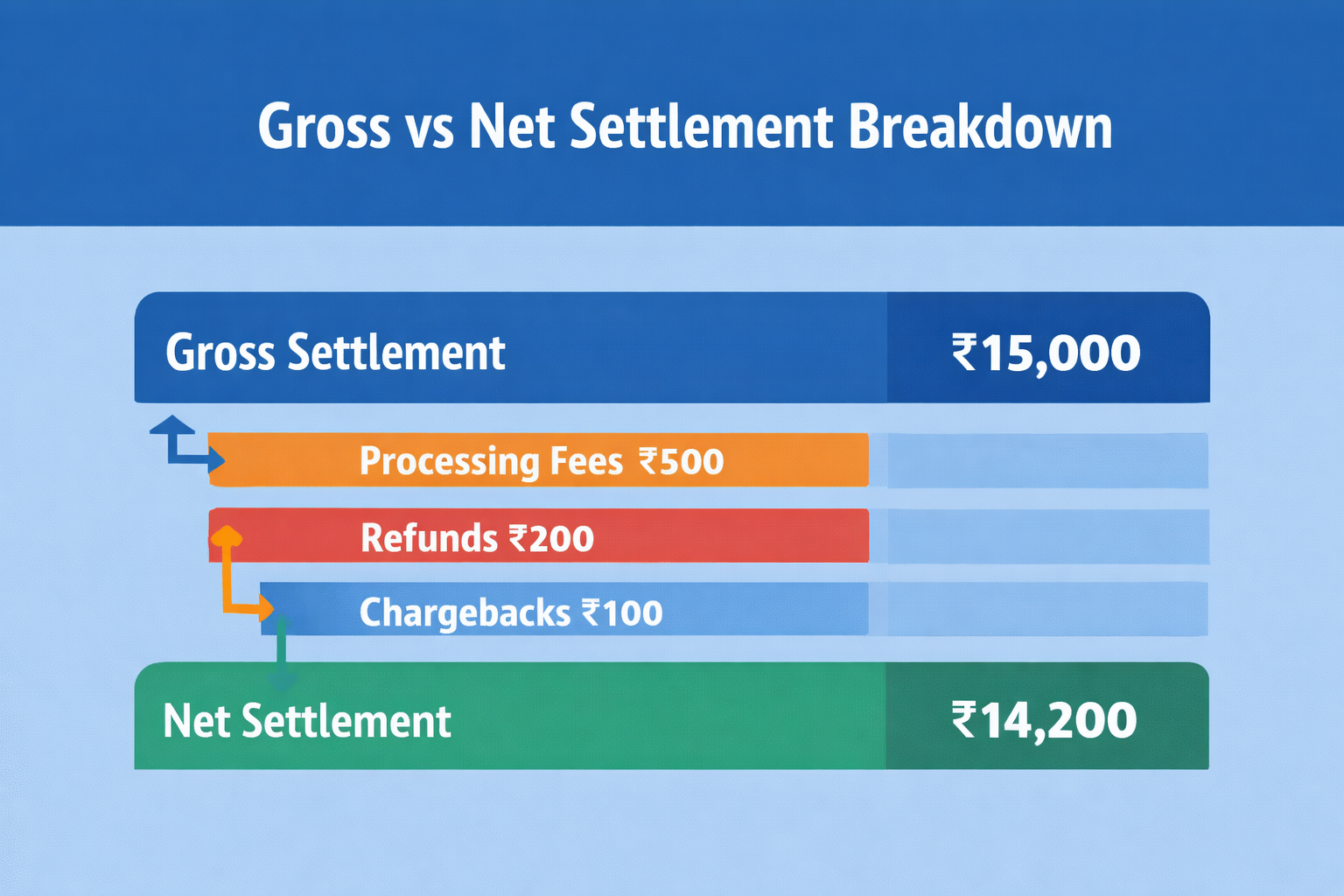

Refunds and Chargebacks

Refunds reduce actual cash received, often on a different day than the original sale.

Chargebacks can pull funds back entirely, along with additional fees.

What Actually Hits the Bank

Your bank receives:

Gross Sales minus Fees minus Refunds minus Adjustments

This is why recording only deposits instead of full sales leads to inaccurate reporting.

A structured system, like SafeBooks’ bookkeeping services, ensures gross revenue, fees, and adjustments are tracked separately.

Third-Party Delivery Platform Payouts and Net Deposits

Delivery platforms add another layer of complexity.

Platforms like Swiggy, Zomato, Uber Eats, and DoorDash:

- Record full order value

- Deduct commissions (often 15 to 30 percent)

- Remit net payouts later

This creates a “double gap”:

- Between POS and platform data

- Between platform data and bank deposits

Additionally, taxes may be handled differently depending on marketplace rules.

If not configured properly:

- Revenue may be overstated

- Tax liabilities may be misreported

- Margins may appear distorted

Restaurants solving this typically move toward integrated systems like those implemented in the restaurant inventory and recipe costing case study, where sales, commissions, and payouts are mapped correctly.

The Hidden Factors Most Restaurants Miss

Beyond timing and fees, several overlooked elements affect reconciliation:

Gift Cards

Cash is received today, but revenue is recognized later. This creates a liability, not immediate income.

Sales Tax

Collected in POS but not always part of usable cash. It must be tracked separately.

Cash Handling

Cash shortages or overages can create mismatches if not tracked daily.

Internal Errors

Incorrect entries, missed transactions, or manual overrides can distort reports.

These are not rare issues. They are common patterns across restaurant operations.

How Restaurant Owners Should Reconcile Daily Sales Correctly

Reconciliation should be treated as a daily control system, not a month-end task.

A structured process includes:

1. Record Gross Sales

Always record full POS sales, not just bank deposits.

2. Break Down Payment Sources

Separate:

- Cash

- Cards

- Delivery platforms

3. Track All Deductions

Record:

- Processing fees

- Platform commissions

- Refunds

4. Understand Settlement Timing

Know when each payment type should hit your bank.

5. Use Clearing Accounts

Instead of matching deposits directly, use intermediate accounts to track money in transit.

6. Investigate Variances Quickly

Any mismatch should be reviewed within 24 hours.

Restaurants that follow structured reconciliation workflows reduce errors, improve reporting accuracy, and gain better control over margins.

Expert Insight

“The mismatch between sales and deposits is not a problem to eliminate. It is a system to understand. Once you map how money flows across POS, processors, and platforms, reconciliation becomes predictable and controllable“

Anshul Agrawal, Accounts Director (CA), SafeBooks

How SafeBooks Supports Restaurant Accounting

If your restaurant is dealing with:

- POS and bank mismatches

- Delivery platform reconciliation issues

- Payment processor confusion

- Daily reconciliation challenges

SafeBooks helps build structured accounting systems that align operations with financial reporting.

Explore solutions for Businesses and scalable Back-Office Support Services, or connect through Contact SafeBooks to evaluate your current setup.