Nonprofits cannot treat every dollar the same. Some funds can be used freely, while others come with rules that must be followed carefully.

Unlike businesses that focus on profit, nonprofits operate on accountability. Every dollar received carries an expectation. If that expectation is not tracked properly, it creates financial, legal, and reputational risks.

What Fund Accounting Means in a Nonprofit

Fund accounting is a system that separates financial resources into different categories based on how they can be used.

Instead of pooling all money together, nonprofits create separate “funds” to track:

- Where the money came from

- What it can be used for

- When it can be used

This structure ensures that every contribution is aligned with its intended purpose and creates a clear audit trail.

Why Nonprofit Accounting Works Differently from For-Profit Accounting

For-profit businesses measure success through profit.

Nonprofits measure success through how effectively they use resources to achieve their mission.

This difference changes how financial reporting works:

- Profit and Loss becomes a Statement of Activities

- Balance Sheet becomes a Statement of Financial Position

- Equity becomes Net Assets (with or without donor restrictions)

Instead of asking “Did we make money?” nonprofits ask:

“Did we use funds correctly and responsibly?”

Organizations that move from basic bookkeeping to structured systems, similar to nonprofit accounting basics framework, gain better control over compliance and reporting.

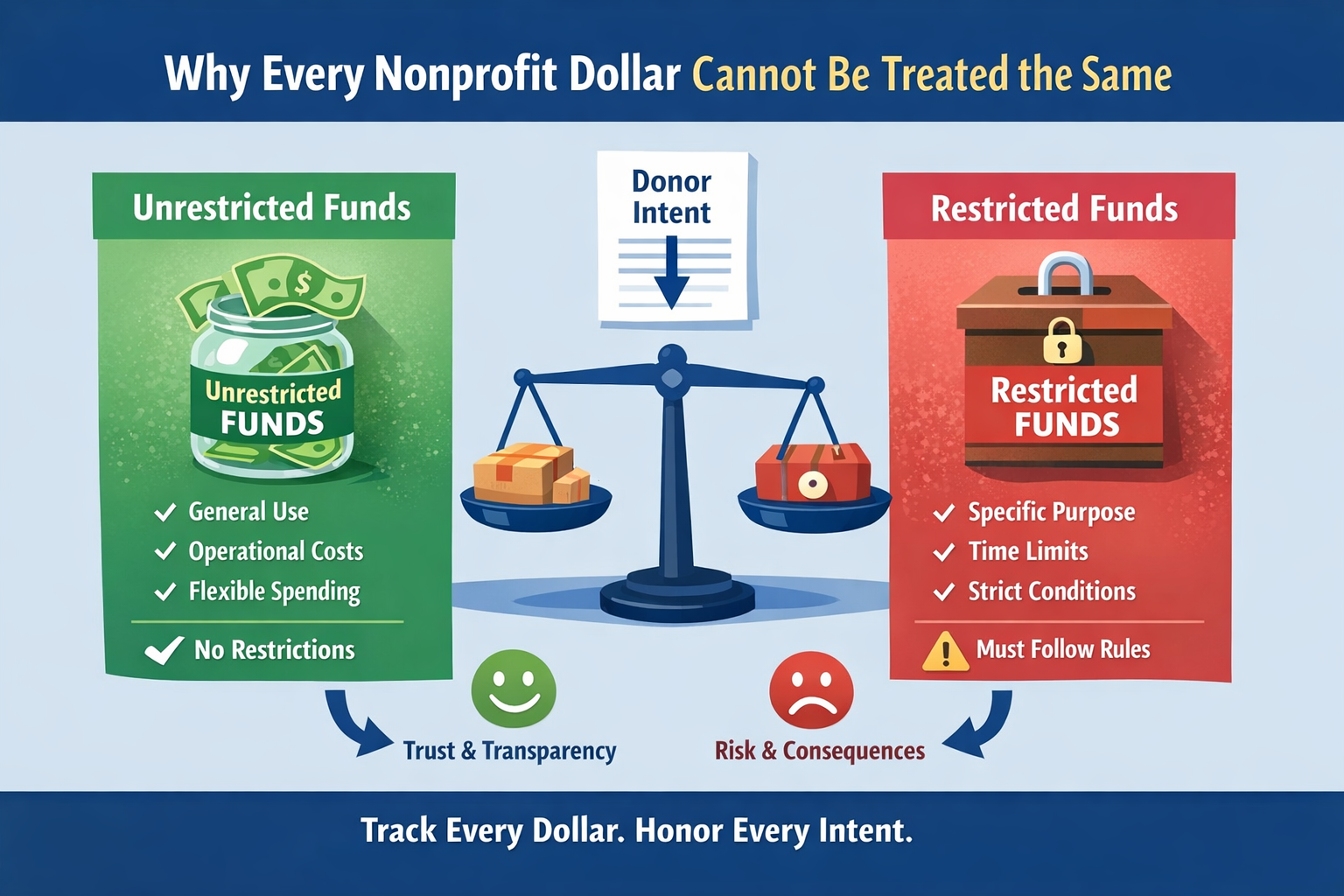

Restricted vs Unrestricted Funds Explained

This is the most important concept in nonprofit accounting.

Unrestricted Funds

These are funds that can be used freely for general operations.

Examples:

- General donations

- Membership fees

- Program income

These funds support:

- Salaries

- Rent

- Administrative expenses

- Operational flexibility

They are often the most critical for long-term sustainability.

Restricted Funds

These funds come with specific conditions set by the donor.

They must be used exactly as intended.

Examples:

- Grants for a specific project

- Donations for a particular cause

- Capital funding for equipment or infrastructure

Misusing restricted funds can lead to:

- Loss of donor trust

- Audit issues

- Legal consequences

Purpose-Restricted and Time-Restricted Funds

Restricted funds are further divided based on how the restriction is applied.

Purpose-Restricted Funds

Funds that must be used for a specific activity or program.

Example:

A donation given specifically for building a school cannot be used for general expenses.

Time-Restricted Funds

Funds that can only be used during a specific time period.

Example:

A donor commits funding for the next financial year or across multiple years.

Key Mechanism: Release from Restriction

Once the conditions are met, funds are “released” and can be treated as unrestricted for reporting purposes.

This ensures financial statements reflect actual usage aligned with donor intent.

Why Tracking Donor Intent Matters

Nonprofits operate on trust.

Every donor expects their contribution to create a specific impact. If that intent is not respected, the consequences go beyond accounting.

Poor tracking can lead to:

- Misallocation of funds

- Audit flags

- Funding withdrawal

- Long-term reputational damage

In many cases, donor agreements act as legal documents. This means compliance is not optional.

Organizations that build structured reporting and tracking systems, similar to financial data protection framework, maintain both transparency and accountability.

Common Problems When Funds Are Not Tracked Properly

Many nonprofits face operational challenges due to weak fund tracking systems.

Common issues include:

- Mixing restricted and unrestricted funds

- Using restricted funds for operational expenses

- Lack of visibility into available cash vs restricted balances

- Incorrect revenue recognition for multi-year grants

- Manual spreadsheet errors and lack of version control

These problems often lead to what is known as a “visibility gap,” where organizations appear financially strong but struggle with actual cash flow.

How Structured Fund Accounting Improves Financial Stability

When implemented correctly, fund accounting helps nonprofits:

- Maintain compliance with donor and regulatory requirements

- Improve audit readiness

- Build long-term donor trust

- Gain clarity on available operating funds

- Make better financial decisions

It shifts the organization from reactive reporting to proactive financial management.

Expert Insight

“Fund accounting is not just about compliance. It is about building trust with donors by ensuring every dollar is used exactly as intended and clearly reported.“

Anshul Agrawal, Accounts Director (CA), SafeBooks

How SafeBooks Supports Nonprofit Accounting

Nonprofits need more than basic bookkeeping. They need structured financial systems that ensure compliance and transparency.

SafeBooks helps organizations:

- Set up fund-based accounting structures

- Track restricted and unrestricted funds accurately

- Manage grant accounting and reporting

- Build audit-ready financial systems

Explore structured support through nonprofit bookkeeping services and scalable solutions via back office accounting support.

If your organization lacks clarity on how funds are being tracked, it may be time to build a stronger system. You can start by reaching out through the SafeBooks contact page to evaluate your current setup.